Most PTAs carry a stack of insurance facilitated by the state PTA they fall under. This typically includes general liability, professional liability, fidelity bond, and workers’ compensation insurance as well as other optional coverage. All together, this insurance protects your PTA against financial liability and loss in the normal and compliant operation of your PTA.

I served as a PTA treasurer for three years across two school districts and trained the treasurers who came after me. Some of the treasurers who onboard to Volo Cash are doing so because in the course of an insurance claim, they discovered that insurance would not actually cover the loss because their books and record keeping didn’t follow the bylaws. This guide lays out what your coverage actually requires, so the records are right before anyone has to test them.

A quick note: the exact policy language, dollar limits, and forms vary by organization and by the insurance program your state and national PTA use. What follows reflects the fidelity bond most PTAs carry and the financial procedures National PTA and most state PTAs share. Always read your own policy and bylaws as the final word.

The coverage that comes with conditions

A PTA carries a small stack of policies, usually bought together through a state and national PTA insurance program: general liability for injuries at events, directors and officers liability for your elected leaders, workers’ compensation, sometimes property coverage, and a fidelity bond, also called crime or embezzlement coverage.

The fidelity bond is the policy tied directly to your bookkeeping. It reimburses the PTA if someone entrusted with its money, an officer, a volunteer, or a member, takes it. It is the safety net under every control in the treasurer’s job. But that bond pays out only if you followed its conditions. The bond most PTAs carry says plainly that if the policy’s conditions are not followed, a claim can be denied, and that it does not cover funds that disappear by mysterious or unexplained loss. In other words, the coverage assumes you kept certain records and ran certain controls.

The fidelity bond is the policy tied directly to your bookkeeping. It reimburses the PTA if someone entrusted with its money, an officer, a volunteer, or a member, takes it. It is the safety net under every control in the treasurer’s job. But that bond pays out only if you followed its conditions. The bond most PTAs carry says plainly that if the policy’s conditions are not followed, a claim can be denied, and that it does not cover funds that disappear by mysterious or unexplained loss. In other words, the coverage assumes you kept certain records and ran certain controls.

Fidelity bond requirements

The fidelity bond most PTAs carry spells out two requirements as conditions of coverage:

- An annual financial review. Your books have to be reviewed each year by an audit committee or a qualified accountant. This is the year-end review most bylaws already require.

- A monthly statement review by a non-check-signer. Each month, the bank statement has to be reviewed and signed by one or more people who do not have authority to sign checks.

Both share the same logic: the people who move the money cannot be the only people who check it. National PTA’s rule on the annual review makes the independence explicit, keeping anyone with signing authority off the review committee. The treasurer is a signer, so the treasurer does not review their own books and does not sign off on their own bank statements.

Syncing your transactions is not a reconciliation

This can be a gotcha with modern accounting tools that automatically sync your bank statements with your books.

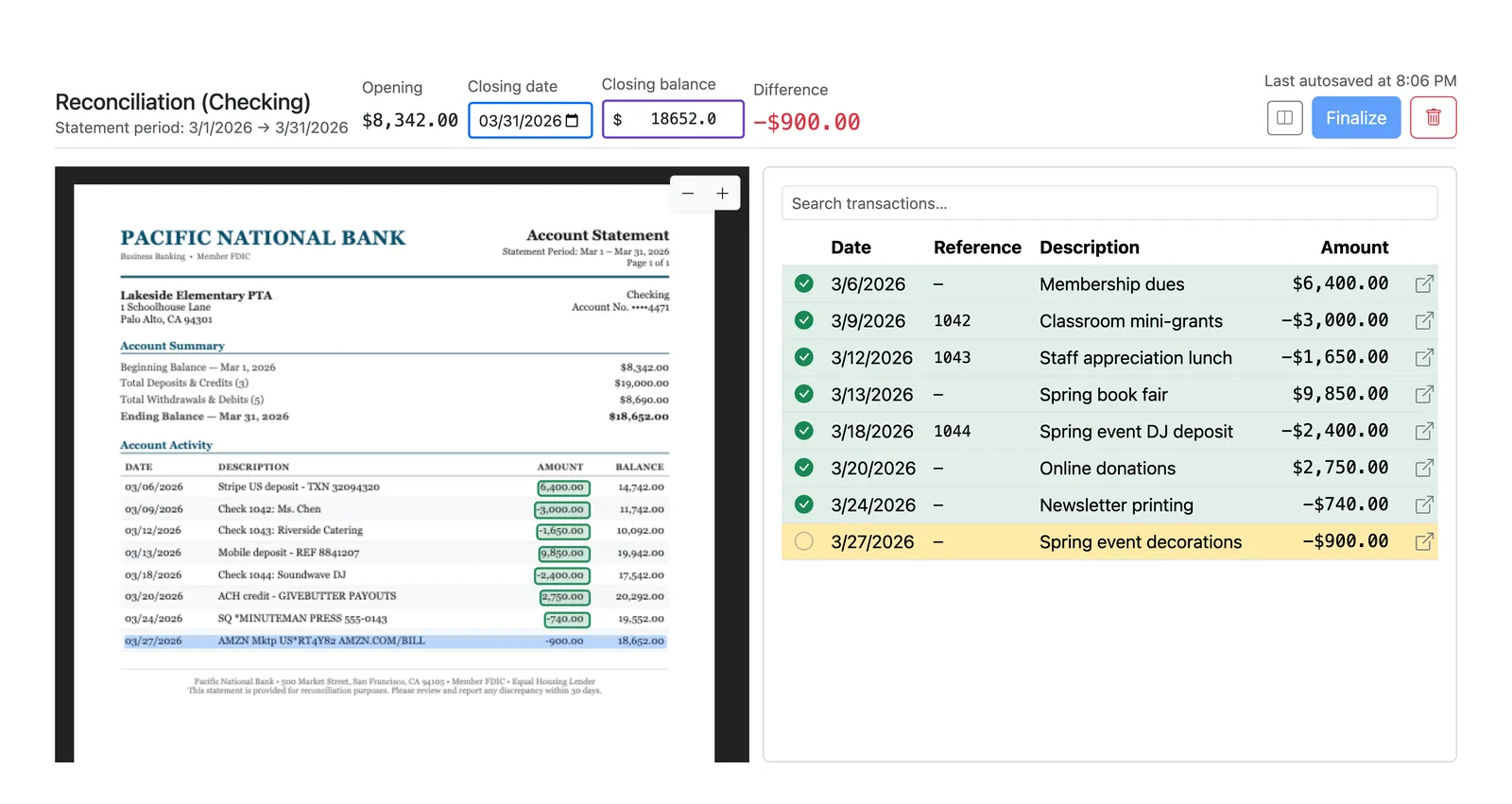

A reconciliation is a specific act: you take the bank’s statement, compare it line by line to your books, and account for every difference until the two agree. It is how you prove that what the bank recorded and what you recorded are the same, with nothing missing, duplicated, or altered.

Many tools, including Volo Cash, offer a bank feed that automatically imports transactions to your books. That is genuinely useful, and it makes keeping your books updated and accurate easier. But importing a feed is not the same as reconciling to the statement, and it is definitely not the same as an independent review. Most requirements are specific: a reconciliation done inside accounting software does not, by itself, meet the requirement. The condition is a human review by someone without check-signing authority.

A reconciliation in Volo Cash: bank statement matching books before routing to a non-signer for electronic review and sign-off.

Best practices to protect against embezzlement

While there are requirements that will be spelled out like reconciliation and annual financial reviews, following your PTA’s financial procedures also ensures a loss is not excluded:

- Two signatures on payments. Two authorized officers sign each payment, and National PTA anchors this to every check. Many PTAs extend the same dual approval to electronic payments, where the two signatures go on a payment authorization instead of on the check.

- Pay by traceable check, avoid cards, and don’t use cash. Checks create a record of the authorizers, payee, memo, and deposit. Credit card transactions are more opaque, and cash carries no inherent record at all.

- Never sign a blank check or a check made out to “cash.” Both remove the control that the two signatures exist to provide.

- Deposit promptly, with two people counting. Undeposited cash is a liability.

- Treat urgent money requests as suspect. A common scam sends an email posing as a board member urgently needing a wire transfer or gift cards. Confirm any request like that in person or by phone, never on the email alone.

Vendors, workers’ comp, and the records you keep

Two more records requirements round out the picture.

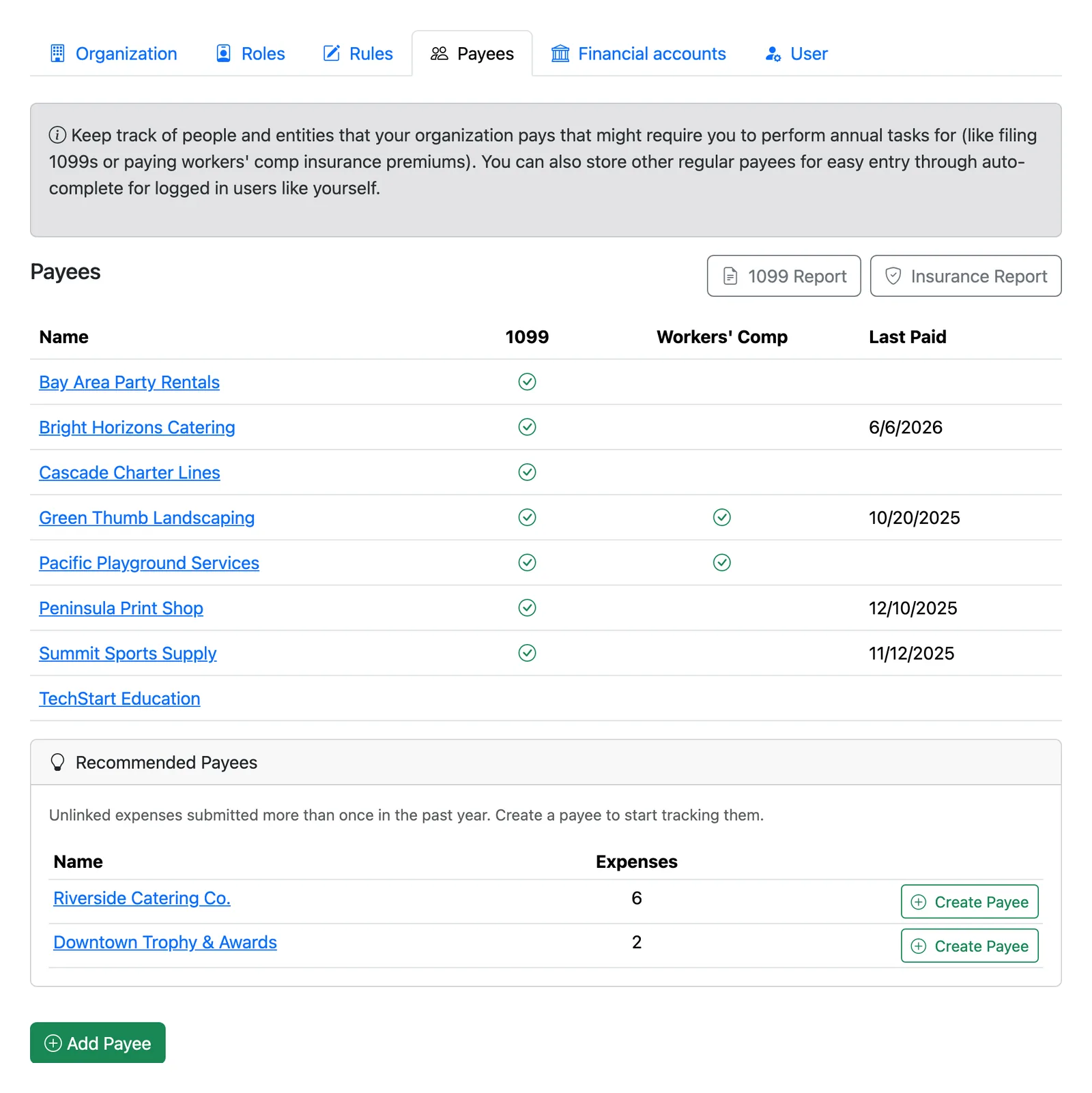

Workers’ compensation and vendor tracking. Whenever the PTA pays a person for their work, like a presenter, performer, or DJ, workers’ comp is in play. Premiums are based on what you paid people and contractors who do not carry their own coverage. So you’ll need to track what each vendor was paid and to collect a certificate of insurance from the ones who are covered. Keep that running as you go, and the annual report is easy.

Volo Cash vendor tracking for annual workers’ comp premiums and 1099 reporting.

Records retention. A claim, an audit, or the IRS can all ask you to produce records, so keep them. Bank statements, reconciliations, and canceled checks are kept for a set number of years, commonly seven. The documents that prove the organization’s history and compliance are kept permanently: the adopted budgets, the annual financial statements, the financial review or audit reports, and the IRS Form 990 filings.

How Volo Cash keeps the records your coverage needs

We built Volo Cash so that meeting these requirements is just how the tool works, not a separate chore:

- A real reconciliation, signed by a non-signer. You match the statement to your books, then a reviewer who is not a check signer reviews and e-signs the finished reconciliation. That is the monthly condition met, with a dated signature on file, not just a matched feed.

- The signatures your bylaws require, on every payment. Volo Cash collects the multiple authorizations your rules call for, even on electronic payments, and keeps the record.

- Vendor, 1099, and workers’ comp tracking. Every payee is tracked with what they were paid, whether they need a 1099, and whether a workers’ comp certificate is on file, so the annual reports build themselves.

- A complete, retained history. Every request, approval, payment, reconciliation, and report is kept and searchable, so when a review or a claim asks for the year, it is all there.

Related guides

- The full job this fits inside, including the annual financial review and the records to keep, is in the complete PTA treasurer handbook.

- The reconcile step in the context of paying people back: the PTA reimbursement process, step by step.

- The year-round rhythm of the controls above: the PTA treasurer duties checklist.

You can try Volo Cash free for three months and set up a reconciliation your reviewer can sign, so the records are right long before anyone has to test them.