A PTA treasurer is the custodian of the organization’s money: you keep the funds and the financial records, pay expenses that have been approved, deposit what comes in, report at every meeting, and file the annual tax return. This guide walks through the whole job, start to finish.

I served as a PTA treasurer for three years across two school districts and trained the treasurers who came after me. When you start, it can feel overwhelming, but it doesn’t have to be. With the right tools and documentation, you can turn the treasurer’s job into something that is easy to manage for yourself and easy to hand off to the treasurer that follows you.

A quick note before we start: what follows reflects the financial procedures most PTAs, PTOs, and booster clubs follow, drawn from National PTA’s finance resources and standard nonprofit practice. The exact form names, vote thresholds, and dollar limits vary from one organization to the next, so check your own bylaws and standing rules.

What the treasurer actually does

The treasurer is the person responsible for the PTA’s funds and its financial records. That responsibility breaks down into a handful of recurring jobs. Depending on the size of your PTA, these responsibilities may be spread across multiple people:

- Help build the budget and chair the budget and finance committee

- Receive and deposit money the PTA takes in

- Pay expenses that have been properly authorized

- Keep an accurate ledger of every dollar in and out

- Reconcile the bank statement each month

- Present a financial report at every meeting

- File the annual IRS return and any state filings

You are the custodian, but you are not solely responsible for every decision. The whole board shares a fiduciary duty to see that the PTA’s money is used the way the members directed. A lot of the controls in this guide exist precisely so that no one person, including you, is ever carrying the whole organization’s money alone.

Taking over the role

Most treasurers start by inheriting the role, not designing it, so the first job is simply getting oriented. Get the bylaws and standing rules and read the financial sections. Meet with the outgoing treasurer if you can. Get the books, the ledger, the checkbook, and access to the bank and any online payment accounts. Contact the bank to update the signature card so the right current officers can sign, which usually means a copy of the minutes from the meeting where you were elected.

Most treasurers start by inheriting the role, not designing it, so the first job is simply getting oriented. Get the bylaws and standing rules and read the financial sections. Meet with the outgoing treasurer if you can. Get the books, the ledger, the checkbook, and access to the bank and any online payment accounts. Contact the bank to update the signature card so the right current officers can sign, which usually means a copy of the minutes from the meeting where you were elected.

For a step-by-step version, see taking over as PTA treasurer: your first 30 days. If you are the one handing the role off, how to hand off the PTA treasurer role walks through doing it well, and how to document the treasurer role covers writing down what you know so you can help improve the process.

The budget: build it, adopt it, amend it

The budget is the PTA’s spending plan for the year, and the membership has to adopt it. The budget and finance committee, which the treasurer usually chairs, drafts it by looking at last year’s actual income and expenses and the programs planned for the coming year. Engage with your program chairs and other board members to include changes they expect for the coming year.

Two votes matter here, and they are different:

- Adopting the budget takes a majority vote of the members present at a meeting.

- Amending the budget later, when a line turns out to be too small or a new need comes up, takes a larger majority in most PTAs, commonly two-thirds.

Both happen at a membership meeting and get recorded in the minutes.

For a walk-through of drafting the plan from last year’s actuals, with a free spreadsheet to start from, see how to build a PTA budget.

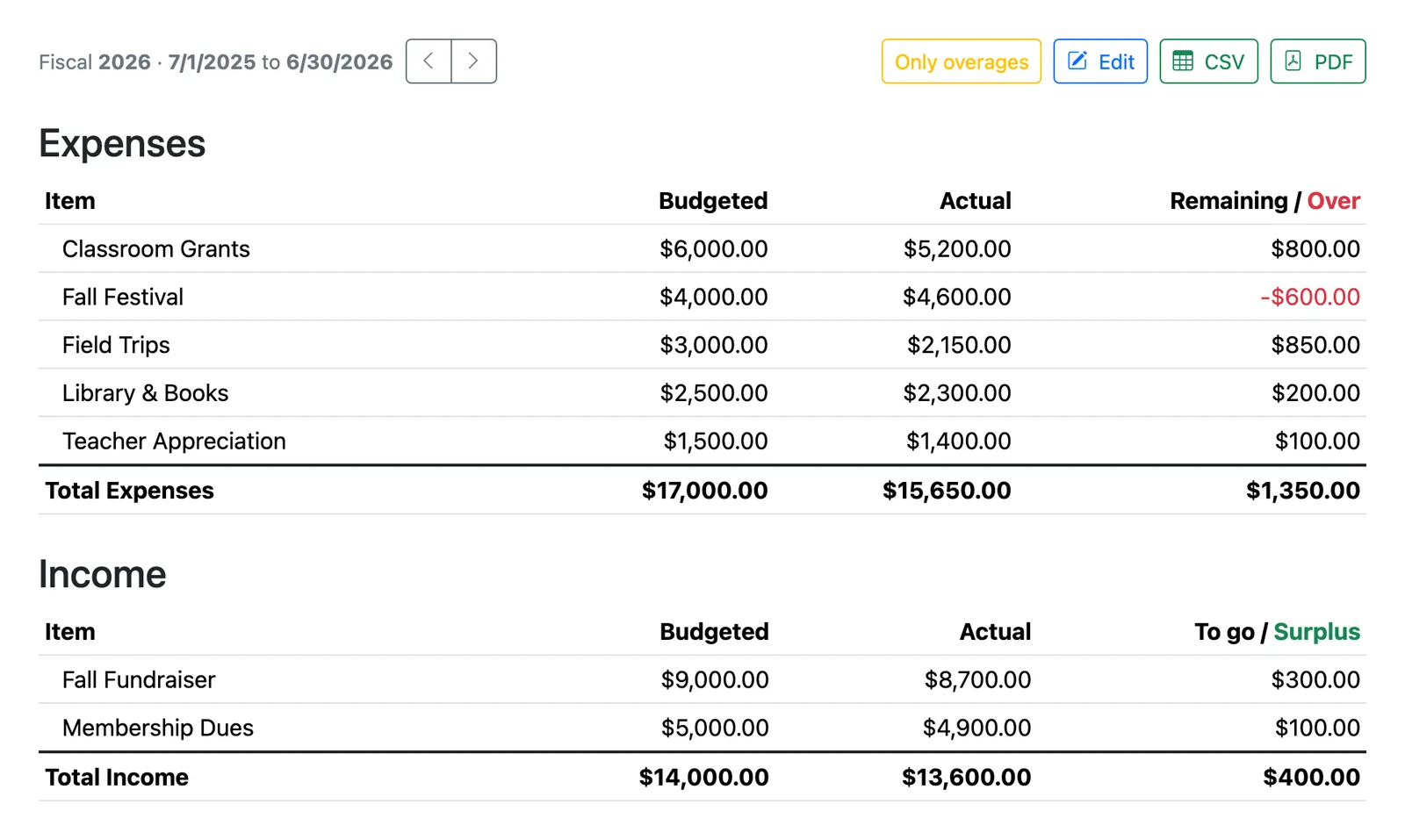

A budget-to-actual report in Volo Cash, with over-budget lines flagged in red.

Paying money out

Paying an expense is a sequence of two main steps: authorizing the expense and releasing the payment. They are related, but different controls.

Paying an expense is a sequence of two main steps: authorizing the expense and releasing the payment. They are related, but different controls.

Authorizing the expense. Adopting the budget does not, by itself, authorize a given expense. The budget is a spending plan; whether you can pay a particular bill comes down to your bylaws. The money still has to be released. Standard procedure comes down to three questions:

- Is the expense within the approved budget, with money still left in that line?

- Has the spending been released, either by the membership at a meeting or by the board within the limit your bylaws set?

- Is there a completed payment authorization form, with receipts attached, signed by the president and secretary?

Releasing funds is usually a motion at a meeting: “I move to release up to $600 for the fall festival.” Or the more generic and open-ended, “I move to release funds required to operate between now and the next time we meet.” Between meetings, your bylaws may let the board authorize spending over a budget up to a set limit with the membership later approving the increase at the next meeting. If you pay money out that hasn’t been properly authorized, depending on your bylaws, you might be on the hook to personally pay back the PTA for the expense.

Releasing the payment. Once the expense is authorized, the payment itself goes out with two authorized signers. This is a different control with a different purpose: no single person should be able to move the organization’s money alone.

A few things most PTA bylaws are specific about:

- At least three elected officers should be authorized to sign, and any two of them sign a given payment.

- The signers cannot be related or live in the same household, and the person being paid can never be one of the two people signing.

- The rule covers electronic payments too. The two signatures can land on an electronic-payment authorization rather than a paper check, which lets you pay through your bank’s bill pay instead of driving a check around for ink.

One practical note: most banks do not actually verify the second signature on a check. So the two-signature rule is really a procedure you document and enforce yourselves, backed up by the monthly statement review and the year-end financial review.

For the full walk-through of paying someone back, see the PTA reimbursement process, step by step. For what belongs on the authorization itself, what to put on a PTA reimbursement form includes a free template. For how authorization should map to what your bylaws say, see how PTA expense approvals should work under your bylaws.

Taking money in

Money coming in has its own short set of controls, and they are mostly about never leaving one person alone with cash. After an event or a fundraiser, at least two people who are not related count the money and both sign a count sheet. Deposit it promptly, in the PTA’s own account, in the PTA’s name. The standing rules of thumb: never take the money home, never run it through a personal account, and never mix PTA money with another group’s or the school’s.

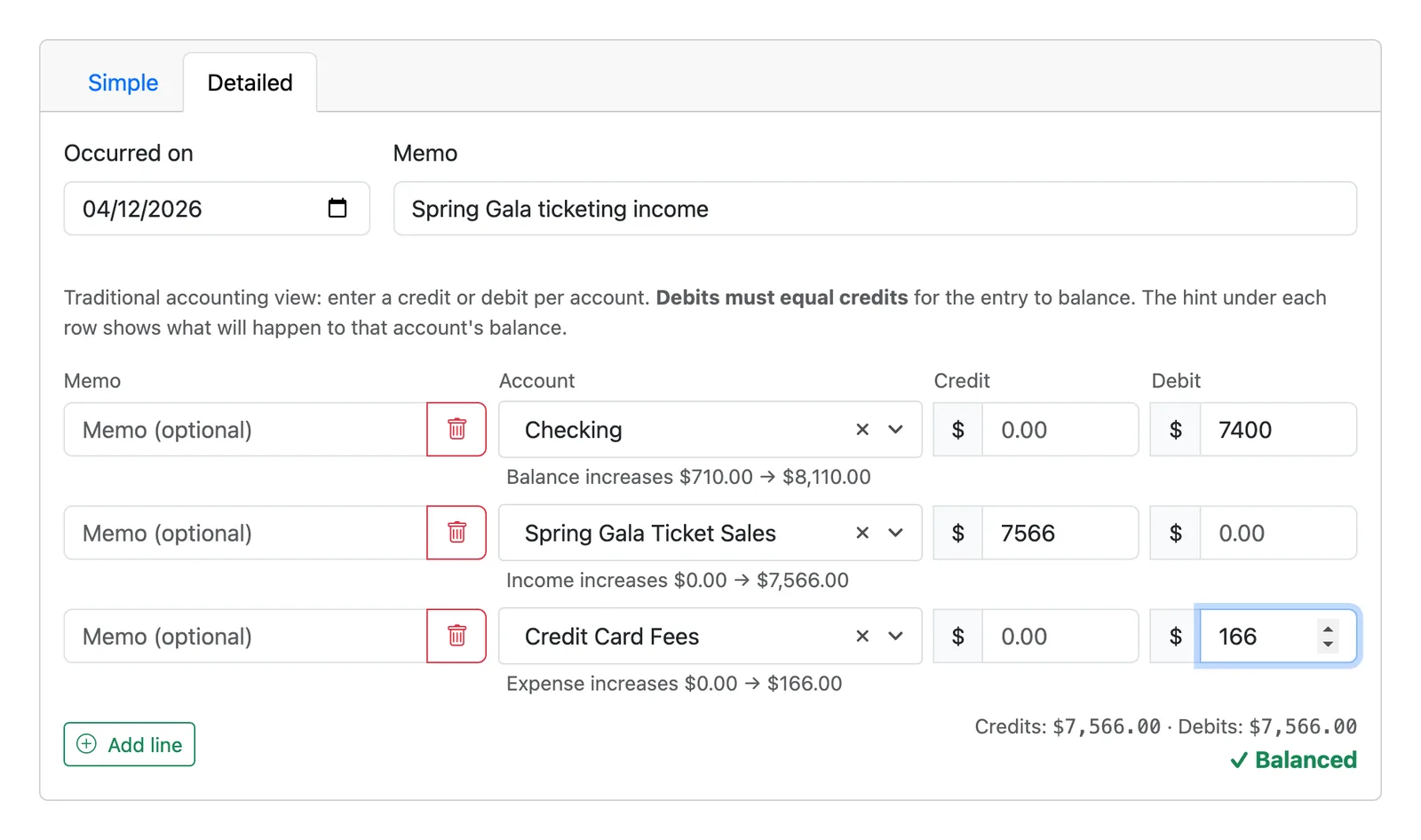

Volo Cash journal entries show you how credits and debits affect different kinds of accounts and categories.

Keeping the books and reporting

Your job between meetings is to keep the ledger accurate and reconcile it every month. A PTA runs best on one ledger that records every receipt and disbursement against its budget line, reconciled to the bank statement as soon as the statement arrives.

The monthly bank statement and reconciliation should be reviewed and signed by someone who is not a check signer, often the financial reviewer. That review confirms two signatures or a documented authorization on every payment and catches errors early.

At every meeting you present a financial report covering the period since the last one: starting balance, money in, money out by budget line, and ending balance. Financial reports are filed, not adopted. The membership does not vote to approve your report the way it votes to adopt the budget. The report is attached to the minutes and kept. Hand the board a budget-to-actual comparison at least quarterly.

The annual financial review

At the end of the year, someone other than you reviews the books. This is the step people call the audit, though many PTAs call it a financial review. It confirms that the money in and money out was documented, authorized in the minutes, and within the budget. For the full walkthrough, when it is triggered, who is allowed to do it, and the records to gather, see how to do a PTA audit.

The key rule is independence. The people doing the review have to be impartial: not the check signers, not the officers who handled the money, not the secretary, and not anyone related to them. They review the year’s records, then report their findings, and the membership adopts the report. A review is also triggered any time the treasurer or a check signer changes, and many PTAs do a second review at mid-year. This review is often what your insurance coverage depends on, which is the next topic.

Taxes, insurance, and records

A PTA is a tax-exempt nonprofit, which comes with a few annual obligations.

The IRS Form 990. Every PTA files one each year, and which version depends on your gross receipts (the amount of money you received in the year):

- Gross receipts normally $50,000 or less: the Form 990-N e-Postcard, filed free online. There is no paper version.

- More than $50,000 and under $200,000 (and under $500,000 in assets): the Form 990-EZ.

- $200,000 or more in receipts, or $500,000 or more in assets: the full Form 990.

The return is due the 15th day of the fifth month after your fiscal year ends, so a PTA whose year ends June 30 files by November 15. Failing to file for three consecutive years automatically revokes your tax-exempt status, by law, with no warning letter. For a step-by-step walkthrough of picking your form and filing it yourself, see how to file your PTA’s 990.

Donations and receipts. Being a 501(c)(3) means most gifts to the PTA are tax deductible, though not always in full. When a donor gets something back, like an event ticket, only the amount above fair market value counts, and every donor needs a receipt with the PTA’s name, date, and amount. Are PTA donations tax deductible? covers tickets, receipts, and why PTA funds cannot be turned into personal gifts.

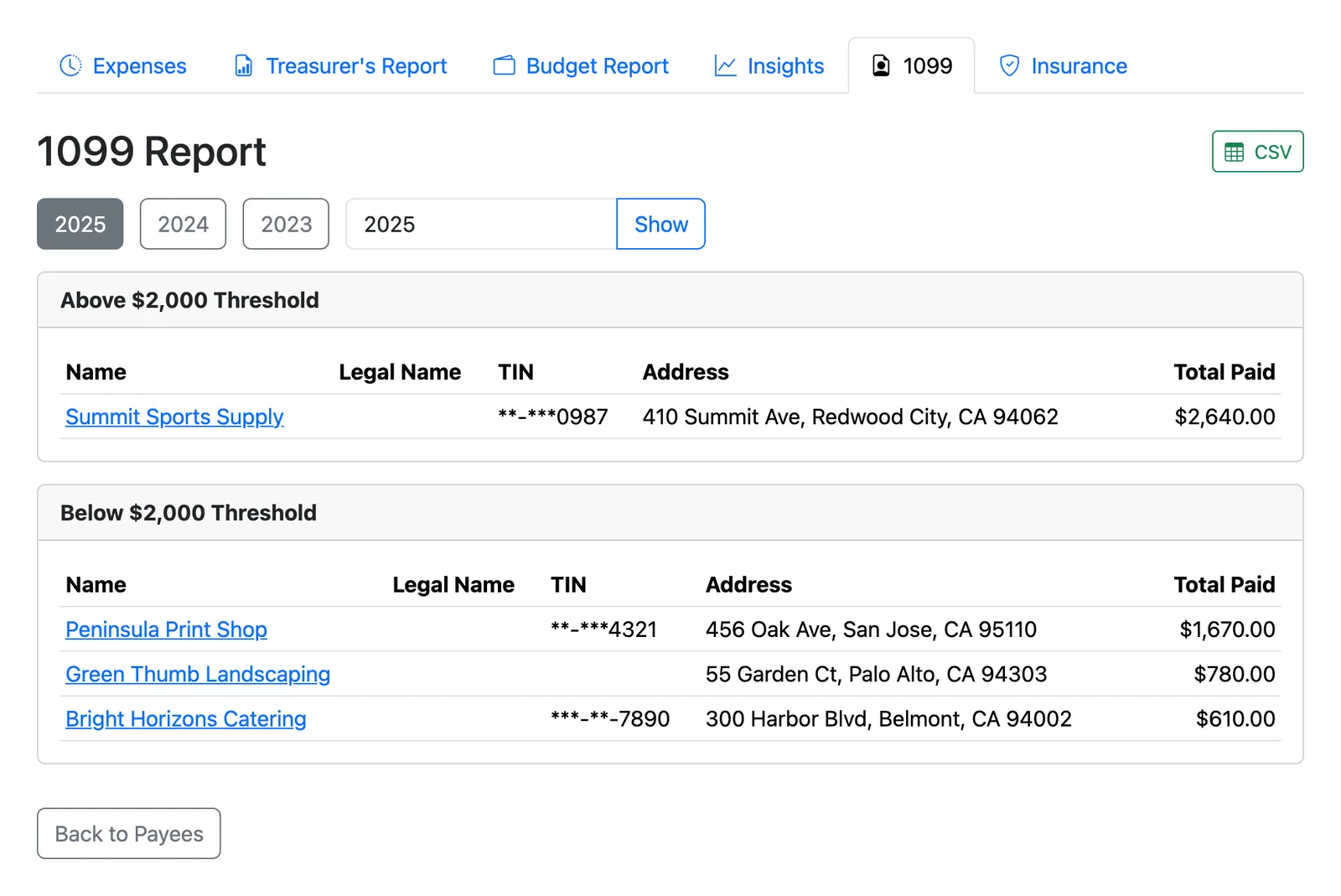

Other filings. If your PTA pays an individual or unincorporated business for services, say a paid presenter or a contractor, you may need to file a Form 1099-NEC. The threshold is $2,000 for payments made after December 31, 2025 (it was $600 in prior years), and the form is due January 31. Your state may also require its own annual nonprofit and charity filings, so check what applies where you are.

Volo Cash 1099 report, grouped above and below the filing threshold.

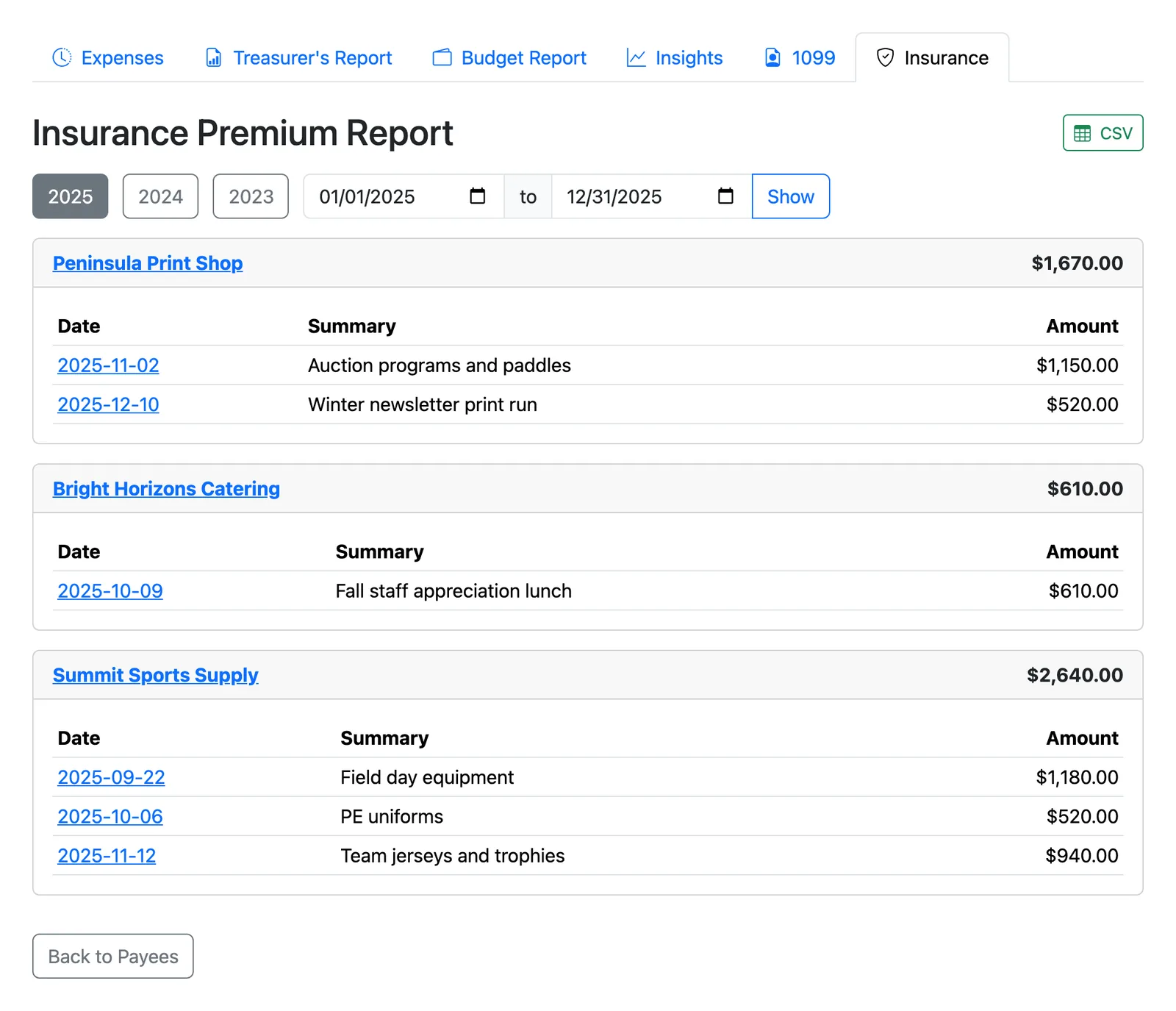

Insurance. Most PTAs carry a small stack of coverage, usually bought together through a state or national PTA insurance program. The embezzlement coverage (a fidelity bond) generally depends on compliant record keeping and following the rules of your bylaws. For the workers’ comp portion of your insurance, you also have to track what you pay each vendor, because those premiums are based on payments to workers and contractors who do not carry their own coverage.

Volo Cash insurance report, totaling payments to vendors without a workers’ comp certificate.

Records. Keep the financial records the PTA is required to retain. Some documents, like adopted budgets, annual financial reports, review reports, tax filings, and the minutes, are kept permanently. Routine items like bank statements and cleared checks are kept for a set number of years. Your bylaws or a records retention policy will spell out the schedule.

The treasurer’s year at a glance

The job follows a yearly rhythm:

The job follows a yearly rhythm:

- Summer: take over the role, update bank signers, get oriented, and start shaping next year’s budget.

- Start of the year: present the financial review of the prior year, adopt the budget for the new year, and file the IRS return for the year that just closed.

- Every month: make deposits, pay authorized expenses, reconcile the statement and have a non-signer review it, and present your report at the meeting.

- Mid-year: an optional second financial review, and a budget-to-actual check.

- Spring: the budget committee builds next year’s budget for the membership to adopt, and you start preparing for the handoff.

For the detailed version of this rhythm, with the specific tasks through the year, see the PTA treasurer duties checklist.

How Volo Cash fits in

Whatever your process looks like, simple or formal, the goal of Volo Cash is to make the treasurer’s job easier without forcing you to change how your PTA already works. It fits the process you have:

- A member submits an expense from their phone with no account to create, picks the budget category, and attaches the receipt.

- You see the remaining balance for that budget line at the moment you approve, so “is there money left in this line” is answered for you.

- It collects exactly the signatures your bylaws require, in the combinations your bylaws allow, and generates the electronic-payment authorization so you can pay through your bank’s bill pay without chasing ink.

- Everything lands in one ledger automatically, so reconciliation becomes matching your bank activity to entries that are already there.

- When a new officer takes over a role, the role and its history carry forward cleanly, and the recurring reminders that go with the job carry forward too.

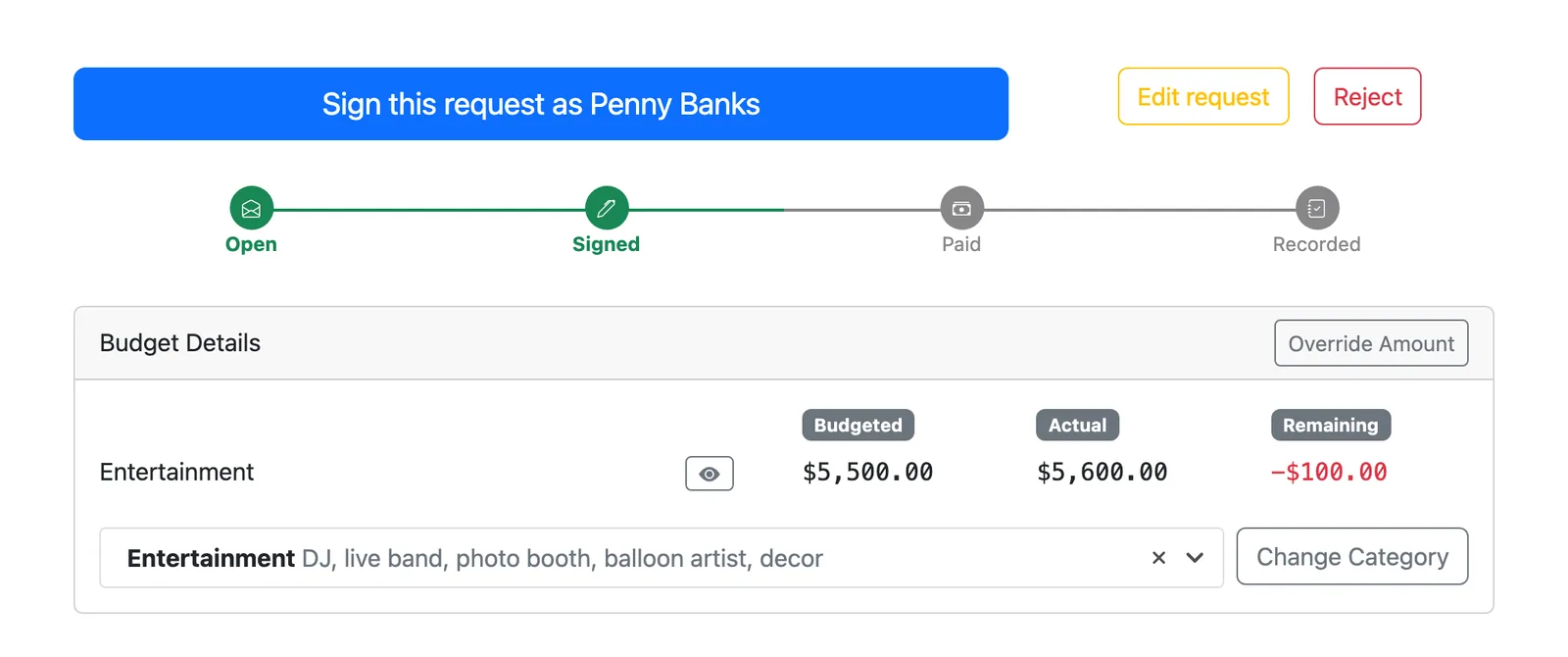

Approving a request in Volo Cash. The budget line’s remaining balance shows as you sign, red when it is over.

And if you are looking to be more official, tighten things up for your year-end review, or add category pre-approvers and dollar thresholds, Volo Cash helps with that as well. The audit-ready trail becomes a setting rather than a project. You can try it free for three months and run your own PTA’s real process through it.

For a wider look at the tools in this space, see the honest roundup of the best PTA treasurer software, or the head-to-head Volo Cash vs MoneyMinder comparison.