Documenting the PTA treasurer role means writing down the recurring work of the job so the knowledge belongs to the position. The role turns over every year or two, and most of what a treasurer knows (when dues are due, how payments get made, what happens in each month) lives in their head. Capture that as an annual calendar of recurring tasks, tie each task to when it is actually due, and the next treasurer inherits a job that explains itself instead of a job they have to reverse-engineer.

I served as a PTA treasurer for three years across two school districts and trained the treasurers who came after me. Good documentation and timely reminders were huge advantages in making sure everything went smoothly, and when I made a mistake or missed something, it was usually because I was too busy to remember what I had to do.

A quick note: the specific tasks and dates below vary by organization. Always check your own bylaws, your state PTA’s procedures, and your local council’s calendar. What follows is the shape most PTAs, PTOs, and booster clubs share.

Why the role needs documenting, not just the books

The books record what happened to the money. They do not record how the job runs. A new treasurer can read a clean ledger and still have no idea that:

The books record what happened to the money. They do not record how the job runs. A new treasurer can read a clean ledger and still have no idea that:

- Insurance premiums are due by a certain date

- The IRS 990-N or 990-EZ is due the 15th day of the fifth month after the fiscal year ends

- Membership dues are remitted to the state and council on a set schedule

- The board expects a treasurer’s report each meeting and a budget-to-actual comparison at least quarterly, plus a full review at year-end

- A particular vendor has to be paid way in advance

None of that is in the ledger. It is institutional knowledge, and in a volunteer org with annual turnover, institutional knowledge is exactly what keeps falling through the cracks.

What to document

Two lists cover most of it: the recurring tasks that make up the year, and the one-time references a successor would otherwise have to reconstruct from scratch.

The recurring calendar

The backbone is a calendar of recurring tasks, each tied to roughly when it comes due. The exact months depend on your fiscal year, but the shape looks like this:

- Start of the fiscal year: finalize the budget and import it into your financial tools; send membership dues; begin preparing the tax filing.

- About three months in: file the IRS 990; have the board complete whistleblower and conflict-of-interest forms.

- About four months in: make any workers’ comp payments; start 1099 prep; begin recruiting next year’s treasurer.

- About six months in: start planning next year’s budget.

- End of the fiscal year: remind everyone to submit outstanding expense requests, then process the ones that come in.

- The transition to the next treasurer: update the bank’s authorized check signers, and prepare for the audit or financial review.

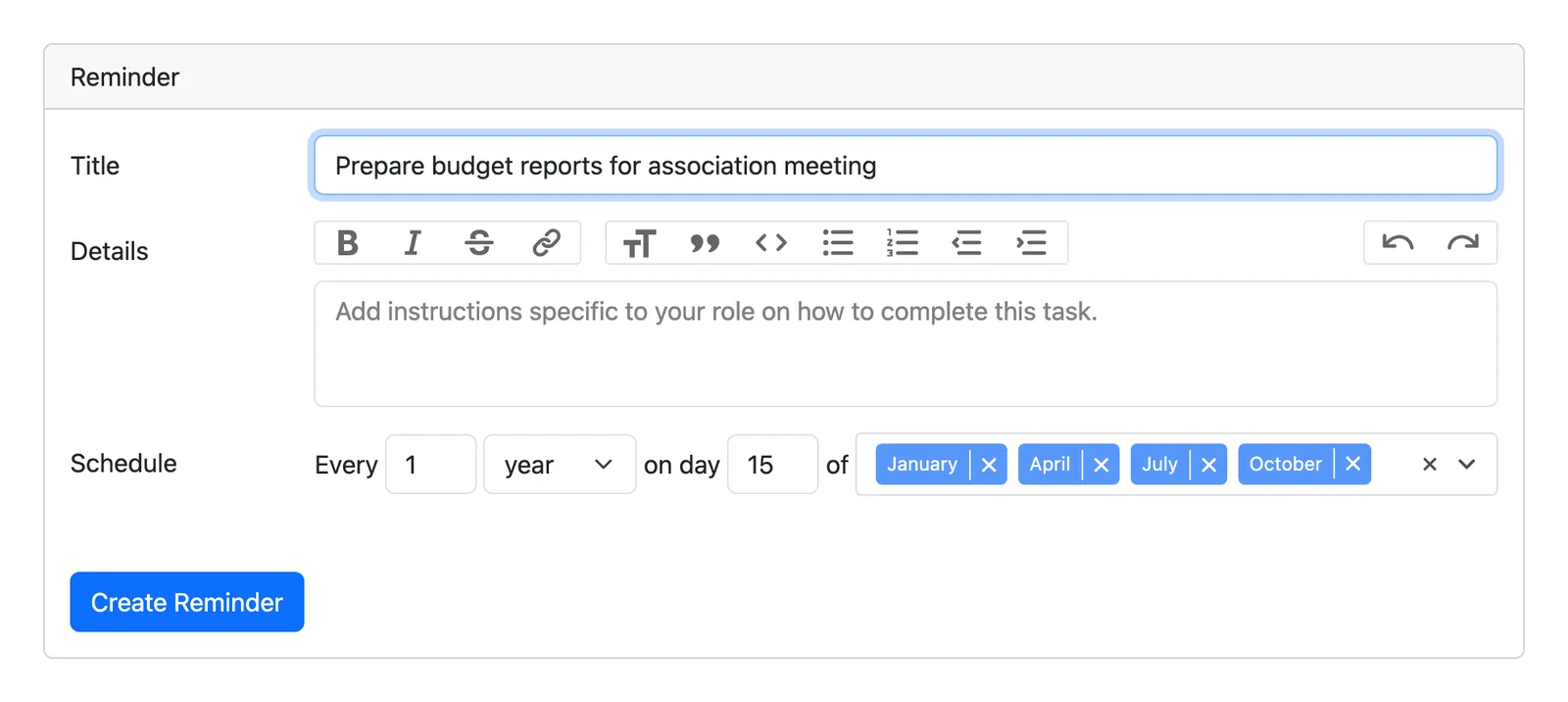

A reminder can repeat on whatever cadence a task actually needs, like this quarterly budget report, so each one lands when it is due.

Creating a recurring reminder in Volo Cash

One-time references

Then there are the things you only have to write down once: the how-tos and account details that rarely change but are painful to rediscover.

- How to order new checks.

- The outside tools, websites, and logins you rely on, such as an auction system, a donor-match portal, or your credit-card processor (note where access lives, not the passwords themselves).

- Your bank accounts and how money moves between them, for example keeping $10,000 of working capital in checking and the rest in a money market account.

- How to reconcile and attribute deposits from a fundraising platform.

- Where the organization’s key paperwork lives: the EIN, the IRS determination letter, the bylaws, the articles of incorporation, and any state charity or sales-tax exemption registration.

- How to make a deposit, including mobile deposit, the endorsement stamp, and any deposit-slip routine.

- How membership dues flow, from who collects them to what gets remitted to your council or state PTA.

- How to produce the treasurer’s report the board expects at each meeting.

- Records retention: what to keep, for how long, and where the archive lives.

- What to do about a bounced check or a stop payment.

Whatever is genuinely specific to your organization belongs here.

The problem with a static document

If you try to record everything in a binder or a shared document, it genuinely helps. But a static document has a habit of going stale, because it tends to sit unopened until something prompts someone to look, and by then the information may be out of date or found too late.

If you try to record everything in a binder or a shared document, it genuinely helps. But a static document has a habit of going stale, because it tends to sit unopened until something prompts someone to look, and by then the information may be out of date or found too late.

The issue is not the writing. It is the timing. A note that says “insurance is due in September” only helps if someone reads it in September.

A better approach: tie each task to its moment

The reliable version of documenting a role is to attach each recurring task to its due date, so the right instruction reaches whoever holds the role at the moment they need it. Instead of one document the new treasurer has to remember to consult, the job surfaces its own steps on schedule: the dues reminder arrives before dues are due, the filing reminder arrives ahead of the IRS deadline, the year-end review reminder arrives in time to schedule it.

That turns documentation from a thing people forget to read into a thing that simply happens on time. And critically, it survives the handoff: the reminders belong to the role, so a new treasurer inherits the whole calendar without anyone having to remember to pass it along.

Where Volo Cash fits

Volo Cash shrinks the documentation problem from both ends. There is less to write down, and what is left becomes reminders that carry themselves forward:

- There is less to document in the first place. How an expense gets submitted, approved, signed, paid, and recorded is the workflow itself in Volo Cash, so there is no procedure to write down and nothing for a successor to relearn. What is left to document is the part that is genuinely specific to your organization: the calendar and the references above.

- Your calendar and references become reminders. Almost everything on both lists can live as a Volo Cash reminder, with recurring tasks set to the dates they come due and one-time how-tos attached where the next person will go looking for them.

- Reminders belong to the role, not the person. Set them up once and they stay with the position. At the annual transition, the incoming treasurer inherits the whole set automatically, so the knowledge does not walk out the door.

- It all lives next to the books. The reminders sit in the same place as your approvals, payments, and ledger, so the calendar of the job and the work of the job are not in two separate systems.

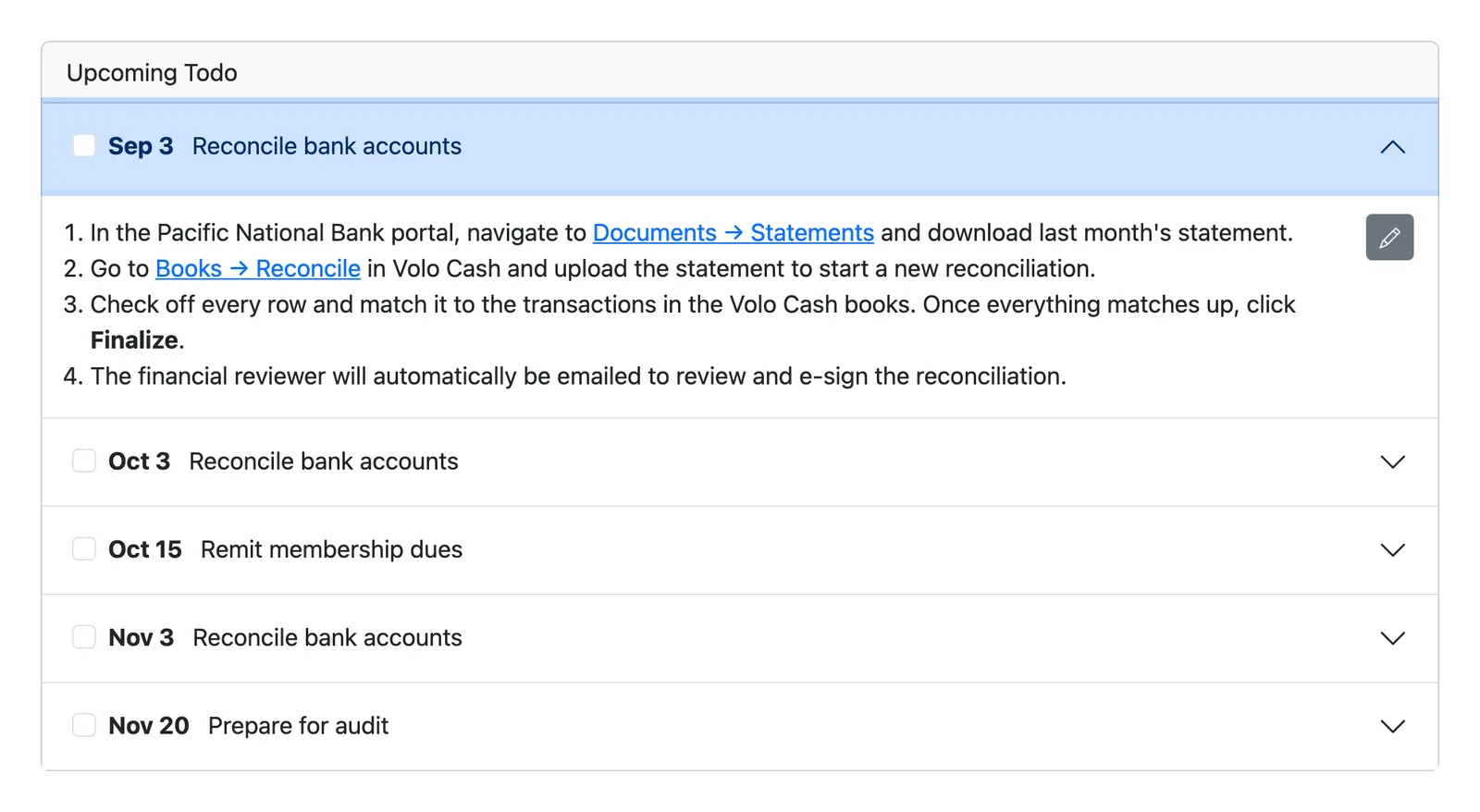

Example reminder todo list from Volo Cash.

Documenting the role this way is a gift to every treasurer who comes after you, and it takes the guesswork out of the job for the one holding it now. You can try it free for three months and set up your treasurer’s recurring calendar so it carries forward on its own.

Related guides

- Taking over the role this year? Start with taking over as PTA treasurer, your first 30 days.

- On your way out? See how to hand off the PTA treasurer role.