A PTA audit or financial review is a year-end examination of the treasurer’s books by members who did not handle the money. Despite the name, it is rarely a CPA audit. It confirms that every dollar in and out was documented, authorized, and within the budget, then reports what it found to the board and membership.

I served as a PTA treasurer for three years across two school districts and trained the treasurers who came after me. I’ve reviewed audit results, prepared other people’s records, followed existing processes, pulled together my own records, and even created new processes. Having your data organized from the start goes a long way to making the audit process easy. The pinnacle in one review was the financial reviewer’s compliment, “I literally have no findings, the records were perfect.”

I served as a PTA treasurer for three years across two school districts and trained the treasurers who came after me. I’ve reviewed audit results, prepared other people’s records, followed existing processes, pulled together my own records, and even created new processes. Having your data organized from the start goes a long way to making the audit process easy. The pinnacle in one review was the financial reviewer’s compliment, “I literally have no findings, the records were perfect.”

A quick note: the exact form names, committee sizes, and deadlines vary by organization and by the state PTA you fall under. What follows reflects the financial procedures most PTAs share. Your own bylaws and standing rules are the final word.

A PTA audit isn’t typically a CPA audit

“Audit” is the common word for this and captures the meaning well. National PTA’s finance guidance calls this section “Conducting an Audit.” Some state PTAs use “audit” throughout their materials, others have replaced it with “financial review” in recent revisions, and a few call it a financial reconciliation. The label varies. The task does not.

But “audit” means something specific in accounting, and that is not what your bylaws are typically asking for. National PTA lays out four ways to have the books examined, in order of cost:

- An internal financial review. Members who do not sign checks examine the records. This is the “free” option, only costing your time, and the one this guide covers.

- A CPA compilation. An accountant assembles your financial statements for you. No assurance is expressed about them.

- A CPA review. An accountant performs limited procedures, less rigorous in scope than an audit.

- A CPA audit. An accountant expresses a formal opinion on whether the statements are fairly stated, the “clean opinion” associated with the word. National PTA suggests this fits state PTAs, very large PTAs, or PTAs required to obtain an external audit by a grantor.

So when your bylaws say the treasurer’s accounts are audited annually, they almost certainly mean the first one.

It is not an IRS audit. An IRS examination of an exempt organization is an external process: an agent visits your premises (a field audit) or asks for documents by mail (a correspondence audit). It is unrelated to your annual review, and nothing about the internal review is an IRS requirement. If a letter ever arrives and says the IRS is conducting a compliance check, you are not being audited. Either way, the fix is the same: keep the records current, and producing them is easy.

When reviews happen

Your PTA may have various events that trigger a financial review, but the most common is the end of the fiscal year. This also tends to coincide with the changing of board positions, and by extension the check signers. It can also be helpful to have a mid-year review so that any recommendations can be implemented and practices can be course-corrected, if need be, by the people who were in position when the changes happened.

Who should do it

Independence is the point, so the rules about who cannot do it are stricter than the rules about who can.

The people excluded from reviewing are, at minimum:

- Anyone with authority to sign checks, which includes the treasurer

- The officers and committee chairs who handled funds

- Often the current secretary and the incoming treasurer

- Anyone related by blood or marriage to those people, or living in the same household as them

- Anyone related to each other, if it is a committee

The common theme: the people who move the money cannot be the only people who check it. That is why National PTA keeps anyone with signature authority, or a relative of theirs, off the committee.

Who can do it depends on your bylaws. It may be an elected financial reviewer, an appointed member, a committee (three or more members is a common floor), or a paid professional the PTA hires. Some procedures let the president serve on the committee as long as the majority are non-signers. Committee members are commonly asked to sign a confidentiality agreement, and the work stays confidential until the report is delivered.

What to hand the reviewers

This will determine how long the review takes; the more organized, the better.

From the treasurer:

- The financial report by category for the period, with the budget comparison (a budget-to-actual report)

- The general ledger, showing every transaction for the period

- The checkbook register, and every check for every account: cleared, voided, and unused

- Bank statements and the monthly reconciliations for every account

- Deposit records with their supporting documentation

- Every payment authorization with its receipt or bill attached

- Monthly treasurer’s reports

- Reports from any electronic payment systems you use

- The IRS Form 990 filing, or the confirmation of acceptance for the 990-N

- Workers’ compensation payroll reporting, and any state or federal forms if the PTA paid employees or contractors

- The report from the last financial review

From the secretary:

- Minutes from membership and board meetings, including the adopted budget, any amendments, the approvals of expenditures, and the ratifications of payments

- The bylaws, standing rules, and any policies in effect for the period

- Membership and board rosters, which let the reviewers reconcile dues collected against the member count

- Any contracts signed during the period

The minutes are the final piece of the puzzle: they show that the budget actions and authorizations were actually presented to and approved by the board and membership. Every expenditure should tie back to a motion in the minutes that authorized it.

What the reviewers actually check

The review is mostly tracing: taking each transaction and following it from the authorization to the ledger to the bank. Standard procedure works through a checklist, and every box that comes back negative becomes a recommendation in the report.

Reviewers start with the records posted after the last review, and confirm the opening balance ties to the ending balance of that review. From there, for the period:

- Every check is substantiated. There is a payment authorization showing the reason, the budget line, the payee, and a receipt or bill.

- The authorization was signed. Standard procedure has the president and secretary sign it, documenting that the expense was actually authorized.

- Cleared checks carry two signatures, both from authorized signers.

- The minutes back it up. The authorization or the ratification is in there.

- Deposits trace through. Each deposit slip matches the bank statement and the register, is properly supported, was counted and signed for by two people, and was deposited promptly.

- Everything is allocated to a budget category, income and expenses alike.

- Bank charges and interest are recorded, not just absorbed.

- Money raised for a specific purpose was spent on that purpose.

- Dues collected match dues forwarded, and the portions belonging to other PTA levels were kept separate.

- The monthly statements were reviewed by a non-signer, if that was not the reviewer’s own job.

- The required filings happened: tax returns, workers’ comp reporting, insurance premiums.

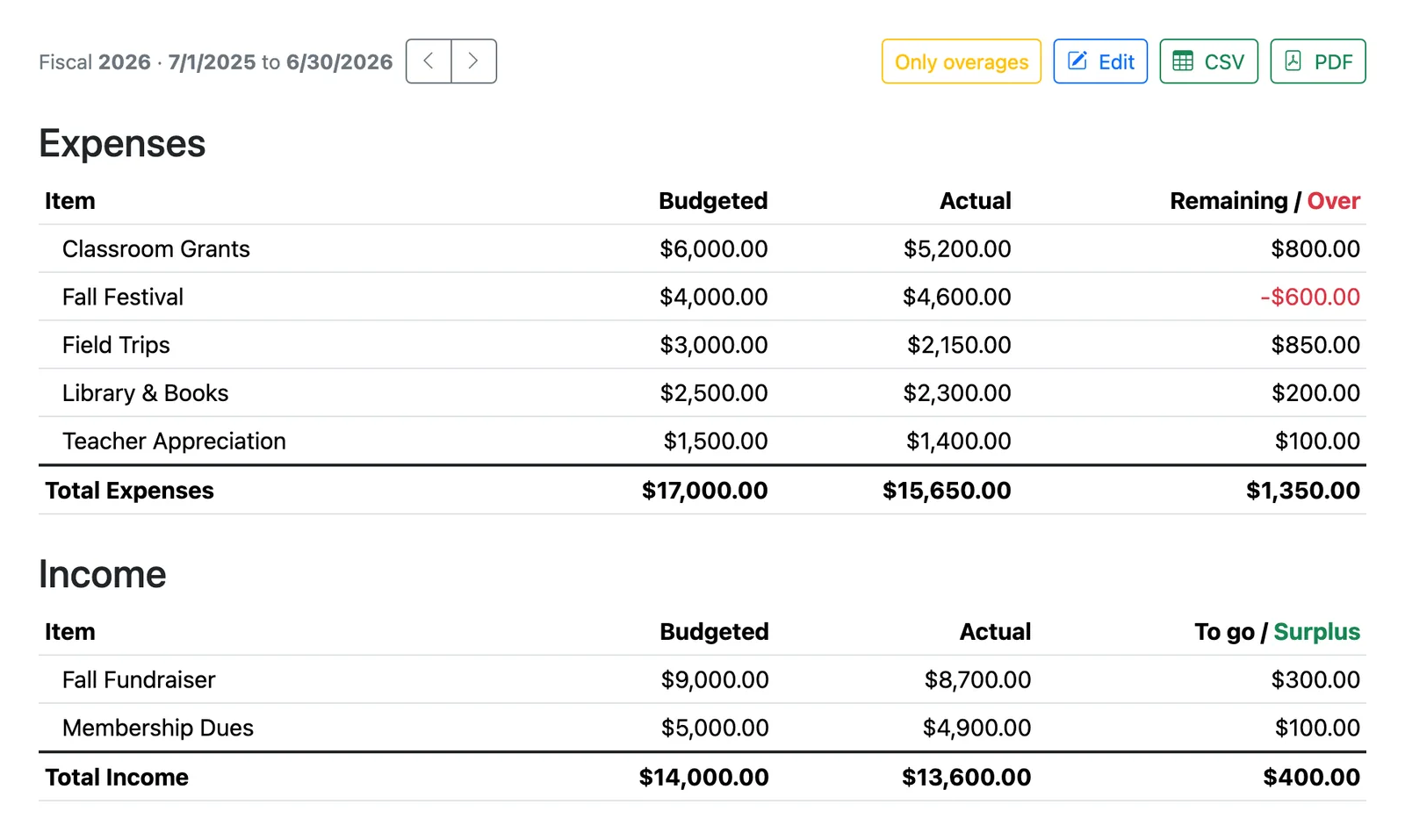

Budget versus actual by line: the comparison the reviewers work from, and the report the membership adopts alongside the review.

Two procedural details. First, reviewers do not fix errors. If they find one, they ask the responsible financial officer to correct it, and the correction gets listed on the next treasurer’s report. Second, in a paper system the review is literally marked in red ink, checked off as it goes, with a double line drawn where the review ends and a dated “Reviewed by” signature.

The report, and the five things it can say

The output is a report with a finding and any recommendations, prepared for each account. Standard PTA procedure gives the reviewer a specific set of findings to read out at the meeting. The records are:

- Correct, with no recommendations

- Correct, with the attached recommendations

- Substantially correct, with recommendations and findings

- Partially correct, meaning more adequate accounting procedures need to be followed before a more thorough review can be given

- Incorrect

Then it moves through the organization in a fixed order: to the treasurer and president first, then to the executive board, which adopts it, then to the membership, which adopts it by motion. The report, the checklist, and the recommendations are retained afterward, permanently in most retention schedules.

It’s helpful to remember: the reviewer should not be punitive, and a difference of opinion about process should not produce a recommendation if the treasurer’s records are correct. The review exists to protect the financial officers as much as to check them. A clean report is a form of cover: it says, on the record and adopted by the membership, that the money was handled properly.

It’s helpful to remember: the reviewer should not be punitive, and a difference of opinion about process should not produce a recommendation if the treasurer’s records are correct. The review exists to protect the financial officers as much as to check them. A clean report is a form of cover: it says, on the record and adopted by the membership, that the money was handled properly.

If the reviewers find something

Most findings are small and procedural, and the fix is a recommendation and a corrected entry. The escalation path when something does not resolve:

- Ask the treasurer or secretary for the missing records or an explanation first. Most gaps are a filing problem, not a money problem.

- If it does not settle, the president decides what happens next.

- Councils and state PTAs will give guidance, and asking early is advised.

- If there is evidence of theft, fraud, or embezzlement, that is a different process entirely. State PTAs have a specific policy for it, the records are retained rather than handed back, and the state office is notified. Your insurance coverage has conditions attached to exactly this moment.

How Volo Cash makes the review short

Whatever your process looks like, simple or highly official, Volo Cash is built to fit it. At review time, everything the treasurer needs to provide is already there:

- Every request already carries its own paperwork. The authorization, the budget line, the receipt, and each signature your bylaws require are attached to the request itself, in one record, with dates.

- Budget-to-actuals report. The comparison the reviewers work from is generated from transactions you already recorded.

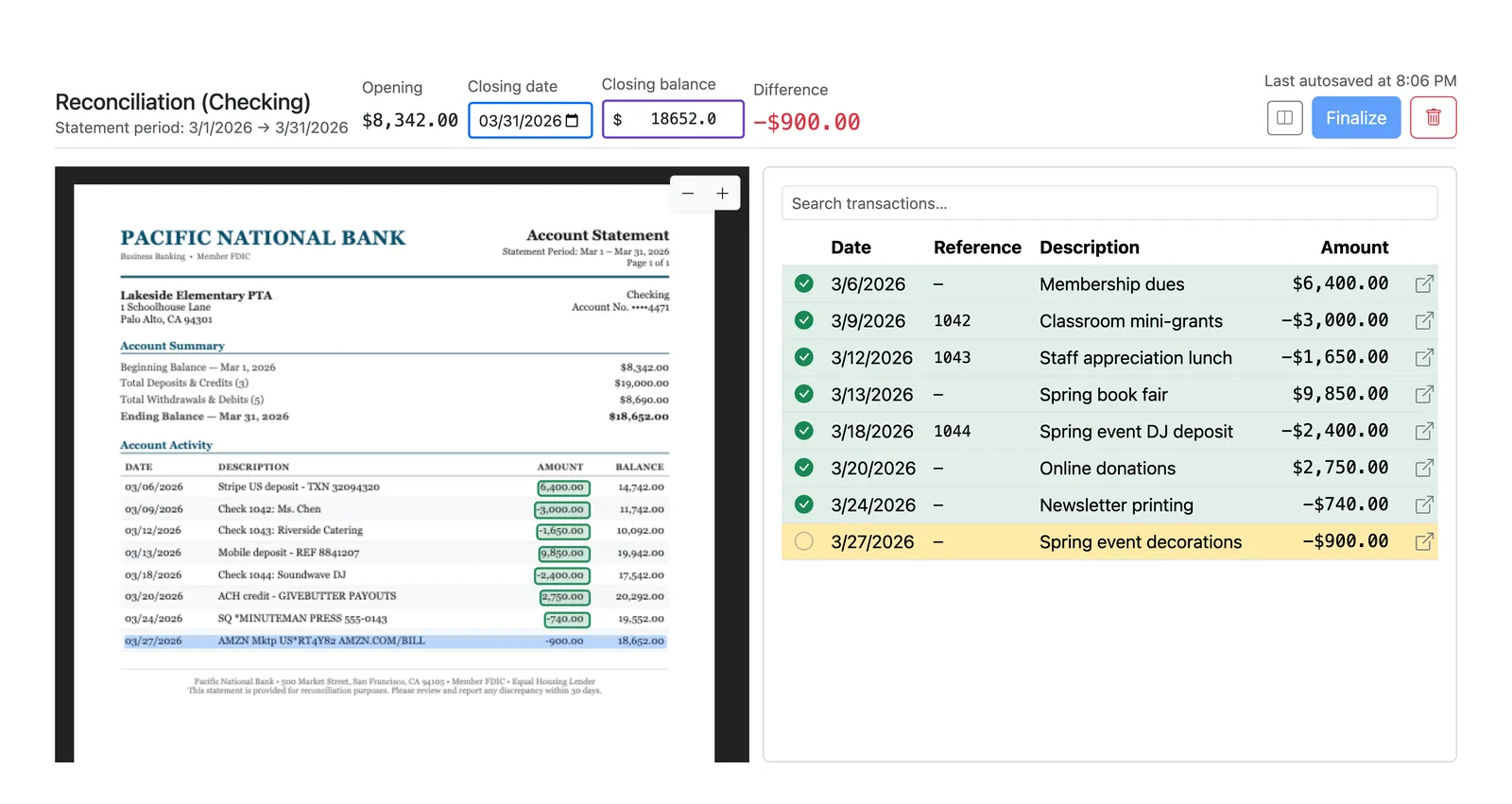

- Reconciliations are signed by a non-signer. After you match the statement to the books, a reviewer without check-signing authority e-signs the finished reconciliation.

- The year is searchable and exportable. When the committee asks for a period, the requests, approvals, payments, reconciliations, and reports are all there.

A reconciliation matched line by line against the statement, ready for a non-signer to review and sign.

Related guides

- The whole job this fits inside: the complete PTA treasurer handbook.

- What your coverage requires from these same records: PTA insurance requirements.

- The authorizations the reviewers trace, from the paying-people side: the PTA reimbursement process, step by step.

- Where the review lands in the year: the PTA treasurer duties checklist.

- A signer change triggers a review, which makes it part of the handoff: how to hand off the PTA treasurer role.

You can try Volo Cash free for three months. Keep the year in one place, and the review becomes a morning instead of a project.